Unlocking Value in Closed-End Funds: Timing & Discounts Matter

Imagine walking into a store and finding a $100 gift card priced at $90, or even $75. Most people would grab it instantly—after all, you’re paying less than face value for something worth more. In the investment world, that same dynamic exists, and it’s called the closed-end fund (CEF) discount.

What Makes CEFs Different

Closed-end funds aren’t newcomers. In fact, they’ve been around since the late 19th century, predating mutual funds by decades. Like mutual funds and exchange-traded funds (ETFs), they pool investor money to buy stocks, bonds, or other assets. But here’s where the paths diverge:

Mutual funds are open-ended. New money flows in and out daily, and managers adjust holdings accordingly.

ETFs trade on exchanges like stocks, but their share count expands or contracts through a creation/redemption process that keeps prices closely aligned with NAV. They’re designed for liquidity and intraday trading.

Closed-end funds (CEFs) launch with a fixed number of shares during an IPO. After that, shares trade on the stock exchange just like any other stock, with no mechanism to issue or redeem shares.

This fixed supply is what creates the unique pricing opportunities investors love, because CEFs can trade at premiums or discounts to the value of their underlying assets. And yes, by “discount,” we mean that the market price of the closed-end fund is lower than the combined value of its underlying holdings — which are themselves actively traded on public exchanges like the NYSE.

Premiums vs. Discounts

Because CEF shares trade in the open market, their price doesn’t always match the value of the assets inside (known as net asset value, or NAV).

Premiums: Sometimes investors bid shares up above NAV. Paying more than the underlying assets are worth is rarely a smart move.

Discounts: Other times, shares trade below NAV. That’s where the magic happens—you’re essentially buying a portfolio of assets for less than their actual value.

The Power of Leverage

Another feature that sets CEFs apart is their ability to use leverage. By borrowing money, managers can amplify returns. While leverage adds risk, it also enables CEFs to deliver some of the highest yields available in the market. For income-focused investors, this can be a game-changer.

Why Now

We’re entering a rare alignment of forces that make CEFs especially compelling:

Interest rate pivot: The Federal Reserve is widely expected to begin lowering rates, with other central banks easing globally. Lower borrowing costs support leveraged funds and income strategies.

Renewed demand for income: After years of chasing growth, investors are rediscovering the appeal of steady monthly distributions.

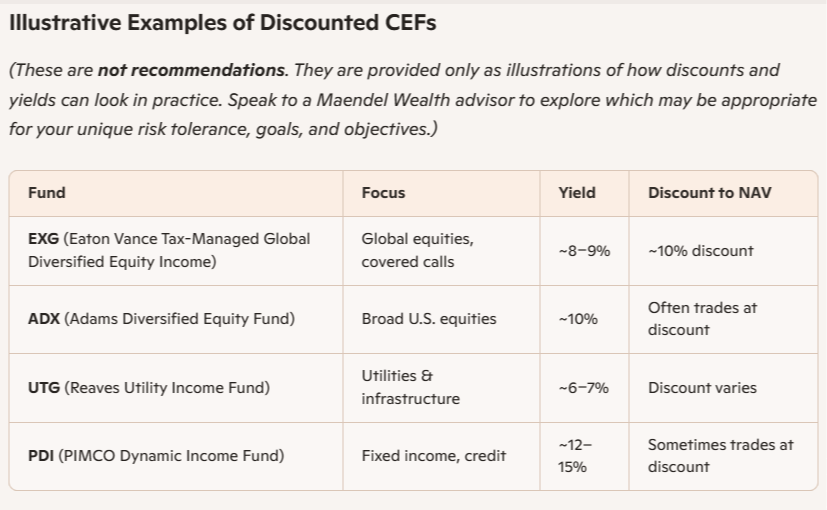

Market correction bargains: The late Autumn 2025 selloff left many CEFs trading at unusually wide discounts to NAV. For disciplined and selective buyers, that can mean locking in income streams at attractive entry points.

Put simply, this is a moment where investors can secure monthly income today, with the potential for capital appreciation tomorrow as discounts narrow and growth resumes. Income becomes the cake, and potential growth the icing.

Beyond Discounts: The Z‑Score

It’s tempting to stop at “is it trading at a discount?” But seasoned investors know that’s only half the story. Some funds always trade at a discount, so the real question is whether today’s discount is wider than usual.

That’s where additional metrics we overlay like the Z‑score come in. Think of it as a way to measure whether a fund is unusually cheap compared to its own history:

A negative Z‑score means the current discount is deeper than normal → potentially a bargain.

A positive Z‑score means the discount is narrower than usual → less attractive.

A score near zero means the fund is trading close to its historical average.

Put simply: discounts tell you if you’re paying less than NAV, but Z‑scores tell you if you’re paying less than usual. That’s how you “load the dice” in your favor.

Final Thoughts

Closed-end funds are often overlooked, but they can be treasure troves for investors who understand how discounts, leverage, and Z‑scores work. With the Fed poised to ease, global monetary conditions shifting, and fresh bargains created by the recent correction, the timing couldn’t be better to explore CEFs as a source of monthly income. For those who want growth potential layered on top, narrowing discounts and market recovery could provide exactly that. And by checking Z‑scores, you can tilt the odds further toward buying when funds are not just discounted—but unusually discounted compared to their own history.

Ready to Take the Next Step?

Need help exploring today’s most promising CEF bargains while avoiding the potential pitfalls? Just reach out to our team via the “Have a Question?” box appearing on most pages of our website, or email James Maendel directly at jmaendel@e-vestech.com. Whether you're looking to lock in monthly income, evaluate Z-score opportunities, or build a portfolio that balances growth and stability, we’re here to help you make confident, informed decisions.

*Please note that nothing here is to be considered individual financial advice. All investments and market prognostications involve some degree of risk and uncertainty. Alway consult a qualified, fiduciary financial advisor and financial planner before making any investment decisions.